Header Title

Smart thinking to end salary slavery?

Time to rethink how a salary links an employee to an employer? Digital opportunities just waiting to be mined …

Away from salary slavery

Payment-for-work structures have remained basically the same for yonks. Simplifying enormously, there are two ways to do it. If you’re an employee of a company or organisation, you probably get a salary (usually monthly) or a wage (usually weekly). If you’re selling your personal services or capabilities to a company or organisation, you send some kind of invoice or bill.

Nowadays, not many of us still get our remuneration in cash in a brown envelope. And there may be all kinds of bells and whistles, fringe benefits, allowances and other line items on top of your salary. But it’s really only the “mechanical” elements of making the payment and the admin details that have changed. Incredibly, the basic structures and presuppositions remain ossified and stagnant. And we still get our payment-for-work as and when the employer company deigns or dictates, within the relevant legislative frameworks and trade union agreements.

Small steps, getting bigger

Employees have very little say in this actual salary disbursement mechanism. It’s usually limited to the appropriate registration of loads of details, and then designating a bank account that the dosh gets poured into as and when the employee and bank jointly permit.

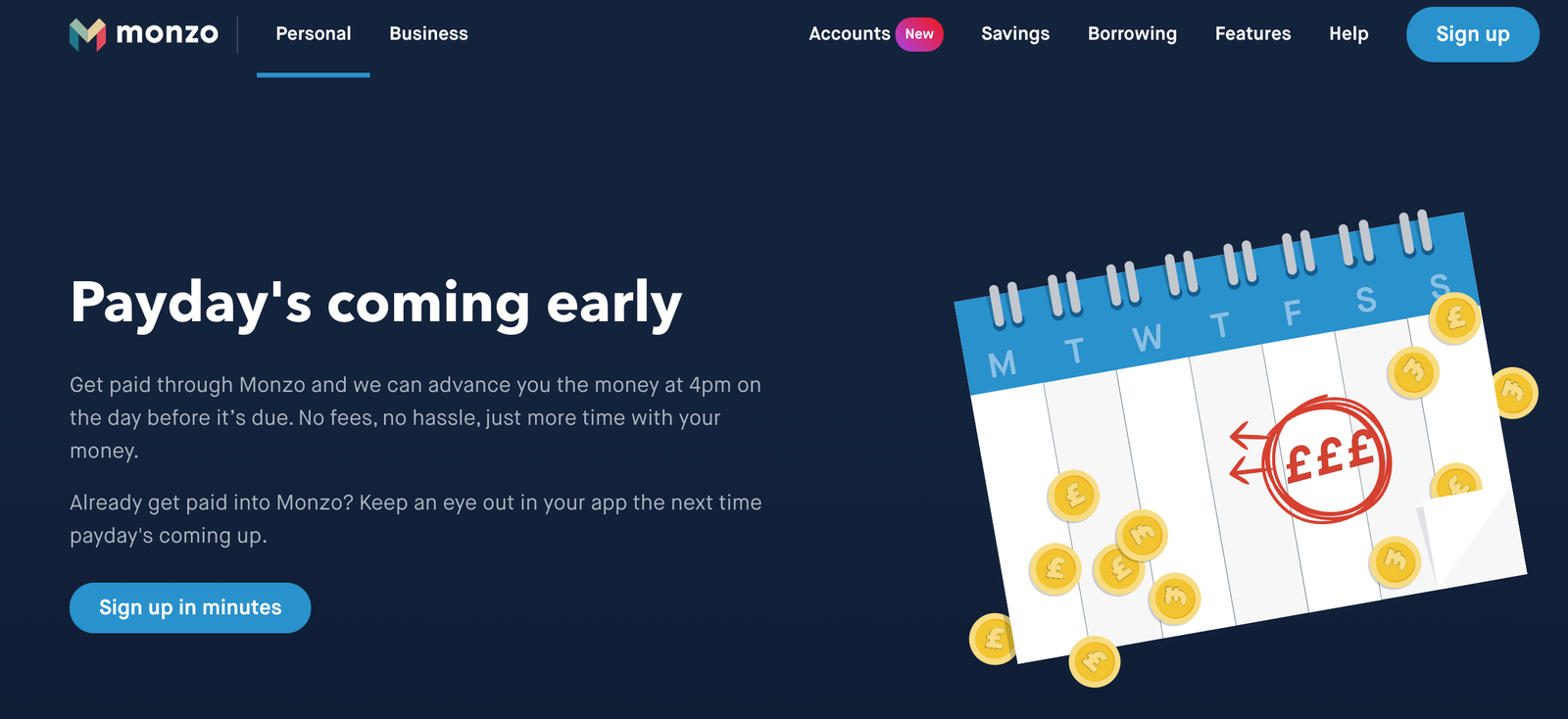

Monzo “Get Paid Early” service

In 2019, however, there was an early microstep towards showing how the emerging neobanking sector could provide some degree of freedom from traditional salary enslavement. UK-based startup bank Monzo (which now runs 5 million+ accounts – it says) launched a feature that enabled its customers to “get paid a day early”, as part of its push to position itself as a bank for people who live via their smartphones, and targeting those who don’t see the need for bricks-and-mortar banking outlets and antiquated-but-still-widely-used-in-the-UK cheque books. The Get Paid Early service is possible because Monzo is able to register a BACS payment (one of the most common types of bank-to-bank transfer in the UK) when it is heading towards a bank account, enabling Monzo to release the funds a day early. Any traditional UK bank could presumably/probably have provided the same service, but it took startup boldness to make it happen.

Liberate salaries

Appropriately named Danish company Salary has taken this idea a whole lot further – and is able to do so by starting from the perspective of being a system for administering companies’ payroll payments. Swipe™ is a feature in the Salary system that enables staff to get their salary paid whenever they want, with a single swipe on their phone.

The Swipe setup is still employer-dictated, in that it is the company that signs up to the service and determines the overall framework, lightens its administrative burdens and takes a step towards ensuring more satisfied staff, by giving them at least an element of self-determination about their own financial situation.

Salary landing page

Rocking individualisation

The key lesson here is that the Salary setup is not a banking system of any kind, but approaches the whole issue from a “salary payments system” perspective. A payroll system must be efficient as well as reliable right across the administration spectrum – and probably also integrate with the company’s financial management and billing systems – thus serving as an essential/integral part of the company’s IT backbone. This paves the way to a much greater degree of digital granularity and greater potential for individualisation than a system based simply on a legacy mindset about shifting pre-defined bunches of dosh from one bank account to another.

Mid-2021 also seem to be an ideal time to make such a leap, as companies and well as employees are realising the potential and benefits of moving beyond traditional, static employment structures and work frameworks post-Covid. New WFH/WFA perspectives don’t match well with traditional clock-punching and employment contracts. In fact, in a world of digital opportunities, it pretty much amounts to head-in-the-sand nincompoopery.

Flexibility to match real-world needs

There’s aren’t many salaried staff whose needs, plans, crises and emergencies automatically fit into rigid monthly blocks, especially if their family dimensions and life quality aspirations are to be taken into account. So why should the transfer of salary-for-work emoluments? Flexible payment frameworks can also help a company protect valuable staff against the notoriously predatory payday lending industry, a seriously big financial services industry that provides high-interest, short-term loans that extract an often-destructively high price from. borrowers.

If deep-digitised intelligently and innovatively, the old-fashioned salary mindset has great potential for transitioning to new degrees of individualisation, and even feature a degree of customisation and self-determination that adapts to changing circumstances and deliver competitive digital user experiences that can give companies a key edge in ensuring staff commitment and brainpower loyalty.

From “how” contracts to “what” mindsets

about self-governance

If a company invests in flexible digital platforms featuring capabilities that can adapt to and be adapted to changing customer habits and expectations, there is substantial potential for delivering digital user experiences that are both competitive and attractive.

If a company is able to provide its salaried staff with a payment framework that aligns with their wider perspectives about managing their family’s finances, planning and quality-of-life goals.

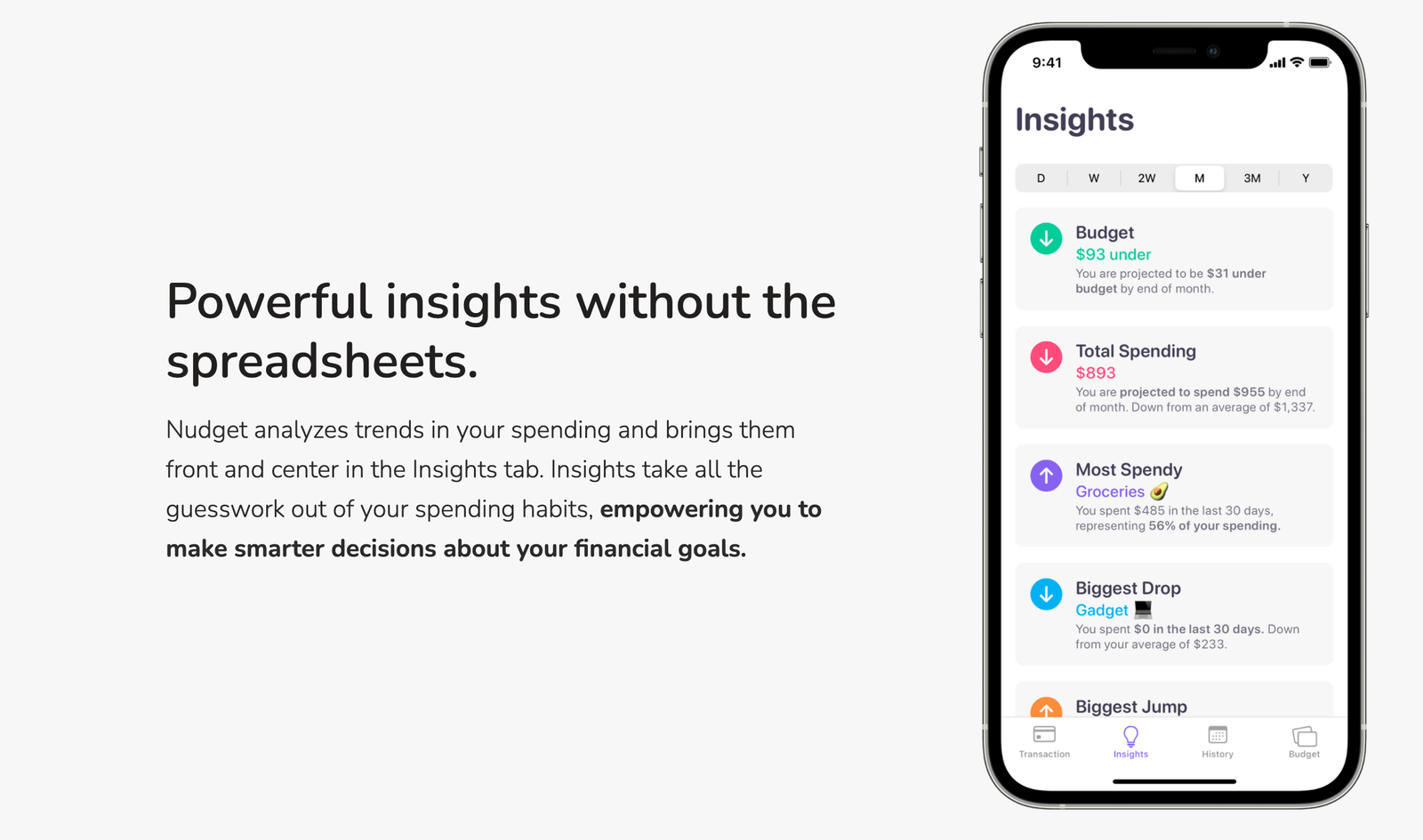

Such digital platforms also pave the way to gamechanger new ways of interacting with staff. Instead of salary payments being held within the realm of remuneration, they might also be extended into the field of behaviour, behavioural management and life conditions. A couple of examples are the Nudget budgeting app and the nicely named Squirrel financial wellbeing company – but there are also countless others, using digital frameworks to achieve a great degree of self-awareness and self-governance. It ain’t just about the salary any more.

Financial self-regulation with Nudget